There seems to be some longstanding confusion about Bitcoin. Not about how it works; there are plenty of articles which explain that quite lucidly— it is confusion about what Bitcoin represents, and what its role could be. I regularly hear these ideas repeated in seriousness:

- Bitcoin could one day supplant ordinary currency

- The decentralized / algorithmic nature of Bitcoin makes it safer than “normal” currency

- Bitcoin is like gold, and gold is good for counting wealth, therefore Bitcoin is good for counting wealth.

I originally penned this article nearly two years ago (before setting it aside). At that time, it seemed like Bitcoin was a passing fad— I believed then, as I believe now, that Bitcoin’s merit (or lack thereof) doesn’t stem from its popularity (or lack thereof), though the mood around Bitcoin has since entirely reversed.

Bitcoin advocates back then would have dismissed Bitcoin’s slide in popularity as proof of its invalidity, though today they’d probably be just as likely to point to its popularity as evidence of its success. I want to cast aside whether Bitcoin is Hot Right Now, as well as questions about implementation details (like the size and existence of transaction fees, the scalability of the blockchain, or transaction delays), and ask whether the fundamental idea is sound. In particular, I think the assertions listed above reveal some really interesting things about the way money actually functions, and what kind of value Bitcoin actually offers. So let’s dive in.

How Bitcoin works

You don’t need to know a whole lot about Bitcoin to understand its basic premise: You have an artificially scarce resource, which in this case happens to be very large numbers with a special mathematical property. That property is what makes the numbers rare, and thus computationally time-intensive to find. As time progresses, the property is designed to become more and more stringent, so new Bitcoin numbers become increasingly difficult to create. The total number of bitcoins in circulation is fixed ahead of time by the algorithm, regardless of how many people are using Bitcoin; and eventually no more bitcoins will be found. Bitcoins cannot be faked, because anyone can verify whether the mathematical property actually holds or not.

Ownership of bitcoins (or parts of them) can be transferred easily, because a large network of computers keeps track of who gave what to whom. There are more technical details which ensure the security of the whole system, but they’re not important to this discussion. What is important is that it is commonly said that this scarcity is what gives Bitcoin its value. And there are some problems with that.

Is Bitcoin like gold?

People often say Bitcoin is like gold and highlight the fact that, like gold, it’s valuable because it’s scarce, and because other people believe it’s valuable.

I’d like to get a small point out of the way: Mere belief isn’t the sole reason for gold’s value. If everyone suddenly stopped caring about how pretty and shiny gold is, it would still have some utility which could be cashed in on. Gold actually has some very useful properties: It’s conductive, it’s extremely malleable, and it’s chemically inert (making it very resistant to corrosion). Assuming its scarcity remains roughly the same, the value of gold can therefore only drop so far, because if the price went down far enough, it would suddenly become profitable to make all sorts of nifty electronics and corrosion-resistant gadgets out of gold, and demand would stop falling somewhere above zero. (1)We can try to get a crude, first-order estimate of the industrial value of gold by comparing it to copper, which has similar properties. If we assume the practical utility— and thus the demand— of gold and copper are similar, then we can estimate the price by comparing the supply. Extracted copper is roughly 6,000 times more abundant than extracted gold, so assuming similar demand, we’d expect the scarcity of the latter to drive its price to about 6,000 times that of copper’s (current) 20 cents per troy ounce. That puts gold’s “utilitarian” price at right around $1200— which is almost exactly its actual current price. Since gold has some additional utility due to its “wealth density”, one of these might be somewhat mis-priced. Gold’s utility beyond a material yardstick of wealth is one thing that lends some credibility to its value.

This is not true for Bitcoin. A bitcoin is a number, and that number has no utility outside of its ability to be accepted by someone else. Unlike gold, the the minimum value of a bitcoin is zero— its value if everyone stops believing it works. This is one reason why a bitcoin is a risky way to hold assets.

This is a common argument against Bitcoin, and I know what many of you are going to say next:

Well, the dollar is the same way, isn’t it?

Yes, just like Bitcoin, the minimum value of a dollar(2)I am going to use “dollar” for the rest of this article to stand in for an arbitrary unit of traditional fiat money. Obviously everything works pretty much the same way for any other currency; feel free to mentally substitute with yours. is also zero, and a dollar has no value outside of its ability to be “accepted by someone else” in exchange for something valuable. So could we imagine a society where BTC is on the same footing as the dollar? Is popularity the only thing distinguishing the two? If both have no inherent value, what’s the difference?

Let’s talk about where the value of currency comes from

Some people still (surprisingly) believe the value of the dollar is backed by gold. This has not been true since 1971, and that is not going to change, either. The dollar is fiat money, which means it has value because the government simply declares it to be legal tender. But the government does not declare its value. The specific value of a currency— like everything else— comes from supply and demand.

It’s pretty easy to understand that if the government were to suddenly double the number of dollars in circulation, the value of a dollar would go down by approximately half. Dollars are suddenly twice as easy to come by, but the utility of everything that dollars are measuring hasn’t changed. That’s the supply side of currency.

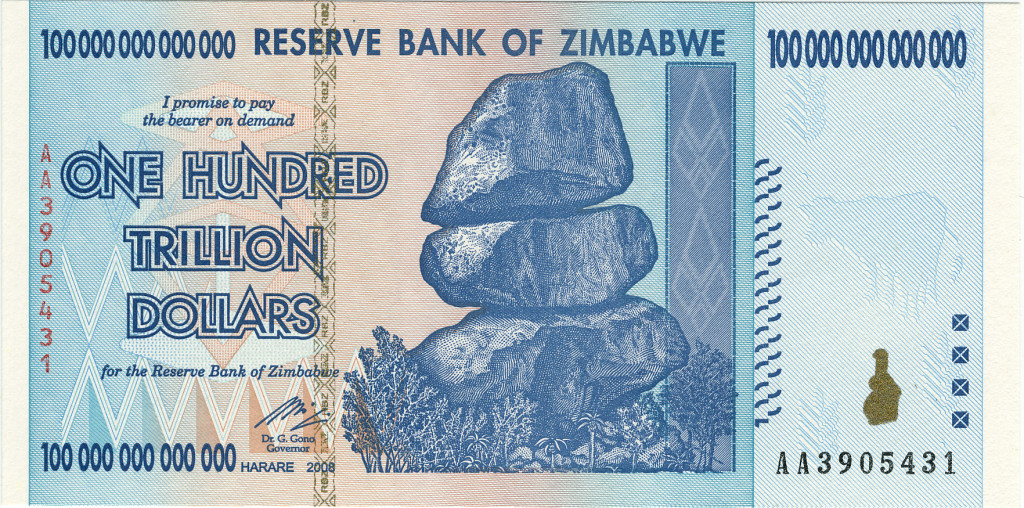

An oversupply of money is the reason why Zimbabwean dollars have to be counted in scientific notation. Cryptocurrency advocates like to point to this sort of thing as evidence for why fiat money is untrustworthy. We’ll look at that idea in a moment.

Post-World War I Germany suffered notably extreme hyperinflation. Here, a woman burns hyperinflated German marks for warmth. Germany’s economy was depressed by the burden of reparations, and it devalued its currency further by flooding the foreign currency market with it. Despite the weak economy and low demand for German marks, the government kept printing notes in higher and higher denominations and increasing the supply. By 1923, a loaf of bread cost over 200 billion marks.

The demand side comes from how attractive it seems to count utility in dollars. If people believe the dollar is unstable, then it might take more dollars to pry someone away from their valuable time or their goods— mainly because they aren’t sure those dollars are going to be worth something in the future. Perhaps other assets (commodities or financial instruments) look more reliable, and become preferable to holding money in dollars. If everyone is trying to shed their dollars this way, or have to give away more of them each time they pay for something, a single dollar gets you less. That’s an example of the demand side; the “belief” that people have in the value of a dollar.

I’ve questioned the first part of that syllogism in the introduction; that Bitcoin is like gold. The second part, that gold is a good currency, is why I’m brining up all this business about how currency gets its value. We’ve seen that currency gets its value from supply and demand, not equivalence to a commodity. So you might be wondering, how did the gold standard work, then? And if it worked, couldn’t Bitcoin work by a similar principle?

What about the gold standard?

Well, it didn’t really work.

Let’s rewind back to 1971, when the western world was still on the gold standard, and the economy was on the verge of collapse. At that time, a dollar grossly mis-mesasured the value of an ounce of gold(3)or rather, 1/35th of an ounce, the equivalence agreed upon in the Bretton-Woods system, because there were far, far more dollars than gold to back them. The mapping of dollars to gold hadn’t been adjusted at all, despite the discrepancy growing for decades in the postwar boom.

In a sense, each ounce of gold held by central banks was being double-counted 100 times over by so many dollars floating around in the economy. That situation was horribly unstable, because it was at huge risk of a panic run on gold— You’d have a lot more wealth if you exchange your dollar for gold; because of the aforementioned double counting, an ounce of gold actually corresponded to a great many dollars. If everyone had realized this and tried to do the exchange, the economy would have been toast.

The situation had been growing worse for some time, and thankfully something was done before disaster struck: The gold standard was abolished, and prices and wages were fixed for 90 days to avoid any panic-induced changes to the economy.

Essentially, the gold standard commits a fallacy by assuming that the value of money comes from the commodity that backs it. In reality, both are governed by separate supply-and-demand forces, and so have separate utility— why should we expect them to move in perfect lockstep, after all? Both Bitcoin and gold suffer from the problem that the amount of wealth you want to measure and the amount of commodity available don’t move in lockstep. Because of that changing relationship between supply and demand, the value of “one unit of currency” must change. Only if they moved in perfect unison would the true value of “one unit” remain fixed.

The gold standard lied and claimed that ratio was fixed, at 1/35th of an ounce of gold per dollar. That lie became more and more egregious as the quantity of wealth to be counted soared away from the amount of gold that was available. It pretended that there was one asset (“dollars and gold are the same”) when in fact there were two.

So for the gold standard, the problem is that the total utility of all the gold in the world is not connected to the total utility of all the goods and services whose wealth needs to be counted. A government declaration that one is exchangeable for the other at a fixed rate can create dangerous market incentives that drive people to hoard one or the other when the true utility of the two start to separate. For Bitcoin, the problem is similarly that the number of bitcoins is fixed, and not connected to the total utility of all the goods and services that need to be counted.

All this points out the fatal flaw in drawing comparisons between gold and cryptocurrency: Gold is a terrible currency to begin with.

So how does the dollar maintain a consistent value?

Proponents of Bitcoin like to point out that the dollar has an unfair advantage: The size of its economy. If the dollar is to change value, truly massive amounts of wealth have to move around in order for a one-dollar fraction of it to have a meaningfully different value.

Bitcoin does not have this going for it; it’s still a small bathtub where every ripple— a million dollars gained or lost— is a big deal, especially when compared to the effect the same ripple would have on the vast ocean that is USD. But that could change: BTC or some other cryptocurrency could massively catch on, and the size of the BTC economy could at least in principle grow to eclipse the size of the dollar economy. This hopefully won’t happen, but it’s not a fundamental limitation of the cryptocurrency concept, and I think many BTC advocates would like to imagine things playing out this way.

But size is only a low-pass filter; it makes it harder for individual players to move the market. The magnitude of the currency pool itself isn’t an inherent protection against a potential panic or runaway inflation— the demand side is still free to move arbitrarily.

The important reason that the dollar maintains its value— and the reason why everyone can believe in its stability and continue to do so— is the Federal Reserve Bank(4)The “central bank”, in general terms.. Demand for dollars is (like anything) organic and capricious, but the supply is directly controlled by the Fed. If the dollar starts to inflate or deflate too much, the Fed can essentially create or destroy money on the spot to bring supply back in line with demand. (As another aside, a lot of people— again, shockingly— believe the Fed does this by handing out U.S. tax dollars. This is not the case; the money is created out of thin air).

This sounds like cheating, but in fact it’s the opposite, since no wealth is being created(5)That happens out in the economy, as people do work, and as buyers and sellers both benefit from their transactions.. The whole point is to make sure that the number of dollars floating around is consistent with the wealth being counted. (Zimbabwe, on the other hand, did cheat— instead of balancing the money supply to match the wealth of the country, it tried to create wealth, in order to pay government officials, by printing money. Obviously this is guaranteed to fail.)

Even if demand for the dollar plummeted, the Fed could in principle (barring Zimbabwean levels of incompetence and corruption) keep burning money until a dollar is scarce enough to be worth the “right” amount. In addition to directly securing the value of the dollar, this capability also reduces the public’s fear the that the dollar could crash uncontrollably, and reduces the incentive to try and get rid of them if the value takes a small dip. This is true as long as the Fed continues to exist and do its job responsibly. Yes, this check could fail, but that possibility is still better than Bitcoin’s complete absence of any check on inflation.

Managing inflation.

And the Fed will continue to exist, at least as long as the U.S. government exists. To bet against this is to bet on the collapse of modern society, at which point you’ll have bigger things to worry about than miscounted wealth, not to mention that you likely can’t count on the availability of WiFi for blockchain access, a free and open internet on which to conduct your transactions, or the massive computational infrastructure needed to propagate the blockchain. In essence, it’s impossible not to found a stable currency on the premise of a stable society.

On the attainability of stable value

So here lies the fundamental difference between the dollar and Bitcoin: The supply of bitcoin is fixed, but the demand is beholden to uncontrollable market forces and speculator whims. That means that unlike the dollar, the value of BTC can never be stable, because there is no means regulate the supply to keep the value consistent from moment to moment. That’s the whole point of Bitcoin: That there is no human being watching or controlling it, which seems like a useful property at first glance (and BTC advocates love to tout it), but it’s a fundamentally flawed premise— it’s human intervention that keeps real money from going off the rails.

It should be clear that any equilibrium is unstable: A sudden random jolt downward in bitcoin price prompts many people to try to sell it and worsen the situation, and the panic itself is worsened since everyone knows there is no check on BTC inflation. This could easily cause the price to spiral permanently to zero, whereas the same situation with the dollar could be readily dampened or halted by the Federal Reserve (as it has been repeatedly). This spiral has played out in Bitcoin’s past, though, and will in all likelihood happen again. At best, a cryptocurrency can hope to avoid this situation out of sheer luck and nothing more.

Of course both kinds of currency are vulnerable to ruin (one from mismanagement, the other from the random whims of the market; both from societal collapse), but a cryptocurrency cannot, even in principle, attain the stability of well-managed fiat currency.

At this point you might suggest that Bitcoin’s fundamental volatility doesn’t mean it’s “not real money”.

This is a good point to talk about why we have money

We’re discussing cryptocurrency’s usefulness as money. So why do we have money in the first place?

The answer is pretty darn simple: A currency is simply a unit for measuring utility to human beings: Utility that we created, utility that we control, utility that we owe. We can divide “utility” into any sized chunks we want; a unit of currency is simply a constant of proportionality— how much utility does one unit of currency measure? We might divide it into large chunks (the British pound) or small chunks (the Yen), but fundamentally we should keep in mind that money is a yardstick for quantifying usefulness.

When you trade somebody for something, you should get something that is approximately as useful in return in order for the trade to be fair. For example, if you sell somebody a hammer for $10, you lose your hammer, but you’ve gotten $10. A fair trade means you haven’t lost anything in the deal, so $10 and your hammer have equivalent utility (6)Really, there must be some difference in valuation in order for a trade to happen— i.e. the buyer thinks a hammer is more useful than the $10 they’re giving up, and the seller thinks the opposite— but for now I only care to illustrate how money measures utility..

If bitcoins were meters

A good currency will keep a stable measure of utility over time. If the utility measured by a single dollar fluctuated a lot, that would mean that the number in your bank account would suddenly miscount the utility of all the work that filled it. Sure, it could be miscounted in your favor, or it could just as easily be miscounted against you. This is very bad because years of utility you’ve created— that rightfully belong to you— could evaporate in an instant simply because the yardstick you’re using to keep track of it all has changed length.

It is not enough if these fluctuations “average out over time,” especially if there is no limit on the inflation or deflation that might happen. Unlike an investment, we need our bank accounts to measure consistent wealth, because we need to know that we can afford bread on Friday, or our rent next month. Similarly, we don’t want to have to “time the market”— to wait for a favorable price fluctuation— to buy necessities, or make regular purchases, or sign contracts. And as we have seen, the need to wait for a favorable market for ordinary activity would likely worsen small fluctuations, as everyone in the economy withdraws or jumps into action at the same time, hoping to avoid an unfavorable miscounting of their wealth.

One way of avoiding this mismeasurement— if you want to keep track of your wealth and you don’t trust your yardstick— might be to individually keep a ledger of all the work that you’ve done for someone else, what each hour entailed, as well as all the items and property you’ve ever sold, all the work others have done for you, and all the property you’ve ever bought. You could compute your “wealth” without money by looking at all the valuable things you’ve ever created or given up (including your time) and comparing their usefulness to all the things you’ve ever received. If you wanted to buy something, you could convince a seller who trusted your ledger that a certain amount of utility (be it actual stuff or work you’re owed) belongs to you, what its value is, and then you could both agree to write in your ledgers that some fraction of it now belongs to him. The next time you try and buy something, your ledger would show you have a little less wealth. A fluctuating dollar or bitcoin wouldn’t hurt your wealth because you’re not measuring things with dollars, you’re comparing them directly.

But this is obviously a huge pain in the ass; the whole point of money is that we don’t have to keep adding up the value of the things it measures; you should be able to count the utility of something once and treat its value as a number that can, ever after, be compared to anything else. This is the very reason why we’re not on the barter system anymore.

Hopefully I’ve convinced you that an effective currency measures predictable utility over time. Money that doesn’t measure utility reliably has lost its fundamental purpose.

All this is why…

It will never make sense for normal people to use Bitcoin like money

For the everyday person not willing to roll the dice on speculation (and not having any strong incentive to hide the movement of their wealth), it does not make economic sense to keep cash in Bitcoin. As we can see from everything above, holding BTC will tend to be very expensive, as large fluctuations can cut your savings in half without warning. And because Bitcoin’s value is inescapably demand-driven, those fluctuations will never go away. The everyday person just wants their cash to accurately count their wealth (not gamble with it), and a fluctuating currency does a particularly crappy job of that.

This instability also makes Bitcoin an impractical medium for transactions: Let’s say you want to pay for something with Bitcoin. Where did your bitcoins come from? Either you kept them in your wallet for an extended time— which we already agree you don’t want to do because of the volatility— or you recently converted them from some other kind of currency. And converting is going to involve a credit card or a bank account or a sketchy Russian BTC exchange or PayPal or Square or something… which is not anonymous, probably involves fees(7)in addition to the built-in BTC transaction fees, and which you might as well have used to conduct the transaction directly. Merchants have similar incentive to convert in and out of Bitcoin as quickly as possible (though they do have some incentive to accept it because it circumvents credit card merchant fees).

If you’re not willing to have a fluctuating bank account, BTC does not make transactions easier. It forces you to make more transactions.

So what is the use of Bitcoin?

Again, we will sweep the current speculative market aside, as the rate of gains we see now can’t persist in the long term.

To hold Bitcoin, it is worth the risk and volatility to people who have strong incentive to hide the movement of their wealth. This includes people buying drugs online, criminal organizations, tax-evaders, bribers and bribees, or governments and political organizations wishing to conceal their movements and influence. Hardcore privacy and cryptography enthusiasts also have non-illicit motivation to hold BTC, but in either case, the incentive to choose Bitcoin has to be strong because (in the long term, on average) it costs real money to hold Bitcoin.

It would also be rational to hold Bitcoin if your belief in the stability of your government is so low that the wild volatility of Bitcoin seems reliable by comparison. This is can readily make sense in unstable third-world countries. We should hope that this will never be the case for the general public in the first world.

The total utility of Bitcoin is then perhaps related to the value of all illicit money, and all the currencies of technologically-equipped nations which are less stable than Bitcoin. (The former also somewhat assumes that governments won’t develop more effective legal and technological techniques for cracking down on the illicit movement of wealth through Bitcoin).

On investing versus speculating

If you look at Bitcoin as a currency, then hoping to get rich by riding its price fluctuations amounts to hoping that your wealth will be miscounted in your favor. That’s a bit like hoping to lose weight by changing the numbers on your bathroom scale: You haven’t got any more or less, you’re just misleading others about it. (And in both cases, that only works as long as you’re the only one using your wonky scale. If everyone uses it, you won’t actually end up fooling anyone).

Or perhaps you are hoping to get rich by waiting for someone else (presumably using the very same reasoning as you) to believe it’s worth more that you did. This might well happen(8)and at the time of writing, it’s happening quite a bit, but not with any certainty. In this case, what you are doing is speculating, and the value of your holding— unlike gold, and unlike a well-managed fiat currency— is floating on air. If Wile E. Coyote opens his eyes, he plummets. And this might be an acceptable risk for a speculator allocating a safe portion of her wealth on uncertain all-or-nothing plays, but it is unacceptable in a currency.

Compare speculating to investing in a stock, for example, where you are hoping that you will become more wealthy because your holdings will become more intrinsically valuable, not merely miscounted: The company will ideally have more customers and make more or better products, or hold more valuable assets in the future; and for those reasons, investors will pay more for the same slice of the company. You’re hoping to own a piece of something that’s useful to people. Investors attempt to distinguish this from speculation(9)Stocks are obviously prone to speculation, too; and that’s where the comparison gets muddy. with fundamental analysis.

If you’re looking a Bitcoin as an investment, then ask yourself: What are you investing in? If it’s your belief that Bitcoin might one day be a major global currency, I hope I’ve convinced you we’re all better off betting against that. If it’s your belief in the growing potential of Bitcoin for concealing illicit money movement, then it’s more likely you’re appraising it by the right metric. And continue to ask: Is that what you want to get behind? How confident are you that Bitcoin can continue to remain under the regulatory radar?

No houses on shifting sand

It’s a very good thing we haven’t built our economy on Bitcoin. Volatility and unpredictability disincentivize investment— big projects require stability over the long term; we have to know that our resources will keep their value long enough to complete the project, and we have to be sure that consumers and tenants will have enough money to buy what we are selling for long enough to pay it off.

Consider also the astronomical spike in BTC price happening now. What would it mean if all our wealth were counted in BTC instead of fiat money? Essentially, we’d be seeing the rapid decrease in supply of money against demand, which manifests as high rates of deflation. All of a sudden, everyone would have no choice but to hoard their money instead of spending it (lest they miss out on the growth), and economic activity would grind to a halt. Intense deflation precipitated the Great Depression, and we’d likely be heading into one right now.

This also highlights how mild inflation is good for the economy: It prompts people to invest their money instead of holding onto it, since there is an opportunity cost in sitting on a currency which slowly loses its value. This is Fed’s way of telling you that it’s better for you to lend your money to someone so they can Do Something Cool with it (like build a business, or public infrastructure) and return it to you at a profit, rather than keeping it all to yourself, where it stimulates no economic activity. On a wide scale, this is essential for economic growth. Inflation is yet another example of a feature of money that BTC advocates mistake for a flaw. The dollar slowly shrinks in value not because the Fed is incompetent; it’s because the Fed is doing its job. It uses this same tool to prod the economy or calm it down when it’s moving irrationally.

If not Bitcoin, then perhaps some other cryptocurrency?

In order for a cryptocurrency to solve the fundamental volatility problem, it would either have to have human oversight (generally considered to be against the premise of cryptocurrency), or build into its protocol the functionality of the Fed.

To do its job, the Fed must estimate— and anticipate— the “belief in” its currency (i.e. the demand), and adjust the supply to correct it. One clue into this assessment is the economic value of all the wealth counted by dollars from moment to moment and year to year; if the pool of money is changing out of proportion to the pool of wealth, this is an indicator that the supply must be adjusted. The Fed has plenty of tools at its disposal to assess this: A deep well of tax and regulatory data, figures on employment rates, trade, imports, exports, financial instruments and currency conversions; a host of economic indicators, as well as qualitative assessments of the economic mood.

Likewise, to match this, a cryptocurrency would at least have to understand and track the economic value of the all goods and services it’s counting. It would either have to mimic the bottom-up wealth-bookkeeping method outlined earlier, or mimic the top-down economic analysis of the Fed. I see no way of doing this without relying on human input, or assessing value in terms of some other good or currency with the same inherent problems that Bitcoin has or is seeking to avoid. Even if there were an algorithm that could do all of this without human intervention, it would have to be built so that it could not be gamed, including if its methods were publicly known.

Since human utility, desire, and trust are things that only humans can assess, the outlook for a completely algorithmic, time-normalized measure of wealth doesn’t look good for the foreseeable future. I suspect that solving this for cryptocurrency would require solving the problem of strong A.I.

The future

Bitcoin is a very clever idea indeed, and it’s very likely we will see more mainstream use of blockchains, decentralized trust, and peer-to-peer bookkeeping in the future— particularly for secure transactions. It seems clear to me, however, that they are not viable replacements for fiat currency.

We learned a lot about managing currencies and economies in the 20th century. Bitcoin reinvents money from scratch, but in many ways ignores those lessons. It’s my hope we can take what’s good about Bitcoin, learn new lessons from it, and certainly not repeat old financial governance mistakes.

Summary

- Bitcoin is not like gold, because gold has intrinsic value aside from its desirability as a means to store wealth.

- Drawing analogies to gold doesn’t bode favorably for Bitcoin anyway, because gold is a terrible basis for currency.

- Bitcoin is not like a dollar, because the dollar is engineered by the Fed to have consistent value over time.

- Bitcoin cannot ever have stable value over time, because without a central bank to manage the money supply, fluctuating demand will drive the price.

- Bitcoin cannot be useful as a major currency, because a major currency must be stable to be effective.

- Bitcoin has always carried an inherent, major risk of collapse, because an unsupervised money supply means that a runaway crash in value is almost inevitable.

- Bitcoin cannot be a serious contender to payment services or credit cards for essentially the same reason that it is an ineffective currency.

- These fundamental limitations of Bitcoin seem to be, at least for the time being, an unavoidable property of all cryptocurrencies.

Further reading

If this is interesting to you, I highly recommend the This American Life episode on “What is money?”

Footnotes

| 1. | ↑ | We can try to get a crude, first-order estimate of the industrial value of gold by comparing it to copper, which has similar properties. If we assume the practical utility— and thus the demand— of gold and copper are similar, then we can estimate the price by comparing the supply. Extracted copper is roughly 6,000 times more abundant than extracted gold, so assuming similar demand, we’d expect the scarcity of the latter to drive its price to about 6,000 times that of copper’s (current) 20 cents per troy ounce. That puts gold’s “utilitarian” price at right around $1200— which is almost exactly its actual current price. Since gold has some additional utility due to its “wealth density”, one of these might be somewhat mis-priced. |

| 2. | ↑ | I am going to use “dollar” for the rest of this article to stand in for an arbitrary unit of traditional fiat money. Obviously everything works pretty much the same way for any other currency; feel free to mentally substitute with yours. |

| 3. | ↑ | or rather, 1/35th of an ounce, the equivalence agreed upon in the Bretton-Woods system |

| 4. | ↑ | The “central bank”, in general terms. |

| 5. | ↑ | That happens out in the economy, as people do work, and as buyers and sellers both benefit from their transactions. |

| 6. | ↑ | Really, there must be some difference in valuation in order for a trade to happen— i.e. the buyer thinks a hammer is more useful than the $10 they’re giving up, and the seller thinks the opposite— but for now I only care to illustrate how money measures utility. |

| 7. | ↑ | in addition to the built-in BTC transaction fees |

| 8. | ↑ | and at the time of writing, it’s happening quite a bit |

| 9. | ↑ | Stocks are obviously prone to speculation, too; and that’s where the comparison gets muddy. |

Thanks for this awesome post! This clarified a lot for me.

Would you say the calculations are different for something like Ethereum, which is meant to run smart contracts? Investing in Ether is really an investment in the utility of running applications on a decentralized network. If, in the future, lots of people want their programs running on the Ethereum network, the price of Ether will go up. I’m not convinced that smart contracts provide too much utility—but at least it seems like more solid ground than Bitcoin. Am I missing something?

Gold has been reserved as the best form of currency for centuries. People and organizations have successfully used gold as a store of wealth and to make large purchases/transactions. By all appearances, Bitcoin will also serve that function going into the future.

Excellent article. Very enlightening. Thank you.

“Bitcoin is not like a dollar, because the dollar is engineered by the Fed to have consistent value over time.” Didn’t read the whole article but why then do we still see inflation of the us dollar over time? Is this by design or inevitable?

“Bitcoin is not like a dollar, because the dollar is engineered by the Fed to have consistent value over time.”

Yeah, author loses a lot of credibility with one sentence. First, the dollar fluctuates in value minute-by-minute on the Forex markets. Second, it has not had consistent value over time, as it has lost over 90% of its value over time.

If you read the whole article you’ll see there’s an extended discussion of this. It is by design. The Fed is very explicit about this: their goal is 2% inflation. Mild predictable inflation helps the economy. A deflationary currency would be a disaster.

Great read. Touches most of the questions I’ve made myself about Bitcoin as a currency.

Interesting. Everything is speculation, at this point, even this article. No one knows how the whole cryptocurrency thing will turn out. I remember reading articles like this in the 90’s about how the Internet was a fad, no one in the right mind would use their credit card online, it’s only good for porn (illicit activities).

Just like the Internet, cryptocurrencies will play itself out and if enough people find it useful, it will catch on.

Appreciate if you can share one of the “articles like this in the 90’s about how the Internet was a fad” — I was not of an impressionable age that time. Thanks.

Nice read.

I don’t want to be rude but ehhhh peripheral vision. Maybe u should rewrite this artikle next year same time.

cheers!

this would indeed be interesting, considering Bitcoin proceeded to collapse.

GOLD will be usable even if there are no thing else;

But with out electricity Bitcoin is nothing.

Stop selling that stupider idea, As I have a even stuiper one;

the whole economy is a lie, nothing really “Value”, we make it “Valueable”

So the gold standard failed in your opinion because there was more claims on the gold than there was gold. So the Gold standard didn’t fail – the counterfeiting caused the gold backed dollar to fail (because they in fact were not backed by gold).

This is precisely what Bitcoin fixes. No counterfeiting. No fakes.

The reasons an excess of IOUs for gold were printed are plentiful: people needed to transact. Governments got greedy. Governments needed money for war. Private Banks issued more currency to try to spur spending. THIS is what caused the failure of the gold-backed dollar that wasn’t really backed.

One of the main issues of gold as money is that there isn’t enough of it to represent every transaction in the world. Sure it’s fine for a micro economy. But you can’t hand around atoms of gold.

Bitcoin is just a ledger (not a “number” as you say). Bitcoin solves that issue by being sub-dividable, so that it can represent every transaction in the world, should it need to.

Bitcoin has a shitload of problems, but this articles misses the mark.

In a way, I agree with you. It is good if we have central banks and someone who controls the wealth of money in circulation. On the other hand, what can you say about the quantitative easing program? Essentially, it is printing money. More precisely, it is (mostly) buying bonds. Central banks are currently pumping huge money into the economy at low (or even negative) interest rates, thus encourage consumption, corporate spending, investing, borrowing and lending etc. But with that they are also creating a huge bubble.